UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2018

OR

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM TO

Commission File Number 0-14710

XOMA CORPORATION

(Exact name of registrant as specified in its charter)

|

Delaware |

|

52-2154066 |

|

(State or other jurisdiction of incorporation or organization) |

|

(I.R.S. Employer |

|

|

|

|

|

2200 Powell Street, Suite 310, Emeryville, California |

|

94608 |

|

(Address of principal executive offices) |

|

(Zip Code)

|

Registrant’s telephone number, including area code: (510) 204-7200

Securities registered pursuant to Section 12(b) of the Act: Common Stock, Par Value $0.0075 Per Share; Common stock traded on the Nasdaq stock market

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ☐ NO ☒

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. YES ☐ NO ☒

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ☒ NO ☐

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files). YES ☒ NO ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

|

☐ |

|

Accelerated filer |

|

☒ |

|

|

|

|

|

|||

|

Non-accelerated filer |

|

☐ |

|

Smaller reporting company |

|

☒ |

|

|

|

|

|

|

|

|

|

Emerging growth company |

|

☐ |

|

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ☐ NO ☒

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the Registrant, based on the closing price of the shares of common stock on June 30, 2018, was $131,035,280.

Number of shares of Registrant’s Common Stock outstanding as of March 4, 2019 was 8,710,797.

Portions of the Registrant’s Definitive Proxy Statement relating to the Company’s Annual Meeting of Stockholders are incorporated by reference into Part III of this Report.

2018 FORM 10-K ANNUAL REPORT

TABLE OF CONTENTS

|

PART I |

|

|

|

|

|

|

|

Item 1. |

1 |

|

|

Item 1A. |

12 |

|

|

Item 1B. |

29 |

|

|

Item 2. |

29 |

|

|

Item 3. |

29 |

|

|

Item 4. |

29 |

|

|

|

|

|

|

PART II |

|

|

|

|

|

|

|

Item 5. |

30 |

|

|

Item 6. |

30 |

|

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

31 |

|

Item 7A. |

39 |

|

|

Item 8. |

39 |

|

|

Item 9. |

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

39 |

|

Item 9A. |

40 |

|

|

Item 9B. |

40 |

|

|

|

|

|

|

PART III |

|

|

|

|

|

|

|

Item 10. |

41 |

|

|

Item 11. |

41 |

|

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

41 |

|

Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

41 |

|

Item 14. |

41 |

|

|

|

|

|

|

PART IV |

|

|

|

|

|

|

|

Item 15. |

42 |

|

|

Item 16. |

48 |

|

|

49 |

||

This annual report on Form 10-K includes trademarks, service marks and trade names owned by us or others. “XOMA,” the XOMA logo and all other XOMA product and service names are registered or unregistered trademarks of XOMA Corporation or a subsidiary of XOMA Corporation in the United States and in other selected countries. All trademarks, service marks and trade names included or incorporated by reference in this annual report are the property of their respective owners.

i

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act, and the Private Securities Litigation Reform Act of 1995, which are subject to the “safe harbor” created by those sections. Forward-looking statements are based on our management’s beliefs and assumptions and on information currently available to them. In some cases, you can identify forward-looking statements by words such as “may,” “will,” “should,” “could,” “would,” “expects,” “plans,” “anticipates,” “believes,” “estimates,” “projects,” “predicts,” “potential,” “intend” and similar expressions intended to identify forward-looking statements. Examples of these statements include, but are not limited to, statements regarding: our future operating expenses, our future losses, the extent to which our issued and pending patents may protect our products and technology, the potential of our existing product candidates to lead to the development of commercial products, our ability to receive potential milestone or royalty payments under license and collaboration agreements and the timing of receipt of those payments. These statements are based on assumptions that may not prove accurate. Actual results could differ materially from those anticipated due to certain risks inherent in the biotechnology industry and for our licensees engaged in the development of new products in a regulated market. Among other things: our product candidates subject to out-license agreements are still being developed, and our licensees’ may require substantial funds to continue development which may not be available; we may not be successful in entering into out-license agreements for our product candidates; if our therapeutic product candidates do not receive regulatory approval, our third-party licensees will not be able to manufacture and market them; products or technologies of other companies may render some or all of our product candidates noncompetitive or obsolete; we do not know whether there will be, or will continue to be, a viable market for the products in which we have an ownership or royalty interest; even once approved, a product may be subject to additional testing or significant marketing restrictions, its approval may be withdrawn or it may be voluntarily taken off the market; we and our licensees are subject to various state and federal healthcare related laws and regulations that may impact the commercialization of our product candidates and could subject us to significant fines and penalties; and certain of our technologies are in-licensed from third parties, so our capabilities using them are restricted and subject to additional risks. These and other risks, including those related to current economic and financial market conditions, are contained principally in Item 1, Business; Item 1A, Risk Factors; Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations; and other sections of this Annual Report on Form 10-K. Factors that could cause or contribute to these differences include those discussed in Item 1A, Risk Factors, as well as those discussed elsewhere in this Annual Report on Form 10-K.

Forward-looking statements are inherently uncertain and you should not place undue reliance on these statements, which speak only as of the date that they were made. These cautionary statements should be considered in connection with any written or oral forward-looking statements that we may issue in the future. We do not undertake any obligation to release publicly any revisions to these forward-looking statements after completion of the filing of this Annual Report on Form 10-K to reflect later events or circumstances or to reflect the occurrence of unanticipated events.

XOMA Corporation (“XOMA”), a Delaware corporation, is a biotech enterprise with an extensive history of discovering and developing innovative therapeutic candidates derived from its unique platform of antibody technologies. In March 2017, we transformed our business model to become a royalty aggregator where we focus on expanding our programs in which we own a right to receive future milestone and royalty payments. These programs and related milestone and royalty interests come from drug candidates discovered by our licensees and partners from their use of our proprietary antibody discovery platform and from product candidates we discovered from that same platform, and advanced prior to out-licensing. In all cases, the licensees have assumed the responsibility for subsequent development, regulatory approval and commercialization. When we transitioned to the royalty-aggregator model we significantly reduced corporate infrastructure in order to minimize the cash burn associated with the period until we expect to experience revenue inflow from these potential milestones and royalties. We expect that a significant portion of our future revenue will be based on payments we may receive for milestones and royalties related to these programs.

Our strategy has a two-part approach to building value. The first component of the strategy is to allow our current pipeline of product candidates to advance over time from the investments made by our licensees. We built this pipeline by out-licensing our technology platform and our drug candidate products to licensees or collaborator partners who assumed the responsibilities of later stage development, regulatory approval and commercialization. We refer to these programs as “fully funded” since our partners pay the development and commercialization costs. As licensees advance these programs, we are eligible for potential milestone and royalty payments. Fundamental to this component is our focus on maintaining an efficient and low corporate cost structure for the reasons outlined above.

1

The second component of our strategy is to expand our pipeline by acquiring potential milestone and royalty revenue streams on additional drug product candidates from third parties. Expanding our pipeline through these acquisitions can allow for further diversification across therapeutic areas and development stages. Our ideal target acquisitions are in pre-commercial stages of development, have an expected long duration of market exclusivity, high revenue potential, and are partnered with a large pharmaceutical or biopharmaceutical enterprise. In September of 2018, we closed our first acquisition and added seven new programs to our fully-funded asset pipeline by acquiring a partial interest position in the rights to potential milestone and royalty payments associated with immuno-oncology antibodies currently being developed by Merck Sharp & Dohme Corp. (“Merck”) and Incyte Europe Sarl (“Incyte”) under collaboration agreements with Agenus, Inc. and certain affiliates (collectively “Agenus”).

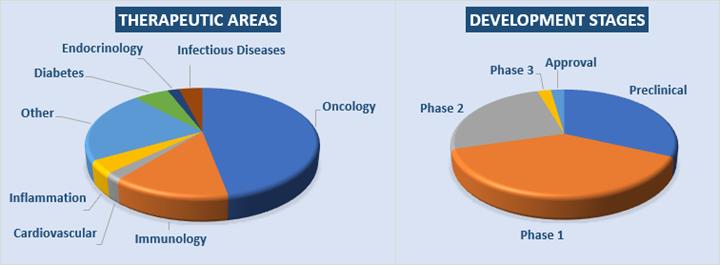

The following charts demonstrate the diversification of our fully-funded asset pipeline across therapeutic areas and development stages.

Selected Programs Underlying Our Core Pipeline

Historically, we have licensed or provided research and development collaboration services to world-class organizations, such as Novartis Pharma AG (“Novartis”) in pursuit of new antibody products under which we are eligible to receive potential future milestone payments and royalties. The following is a summary of material license and collaboration agreements that represent a significant component of our core pipeline.

Novartis – Anti-CD40 Antibody

In September 2015, we and Novartis Vaccines and Diagnostics, Inc. (“NVDI”), further amended our 2008 Amended and Restated Research, Development and Commercialization Agreement, relating to anti-CD40 antibodies. Under this agreement, NVDI is solely responsible for the development and commercialization of the antibodies and products containing the antibodies arising from this program. The parties agreed to reduce the royalty rates that we are eligible to receive on sales of NVDI’s clinical stage anti-CD40 antibodies (“CFZ533”). These royalties are tiered based on sales levels and now range from a mid-single digit percentage rate to a low double-digit percentage rate.

Our right to royalty payments expires on the later of the expiration of any licensed patent covering each product or 10 years from the first commercial sale of each product. Novartis is conducting early clinical testing of CFZ533 in several indications.

Novartis – Gevokizumab and IL-1

In August 2017, we and Novartis entered into multiple license agreements. Under the first license agreement (the “XOMA-052 License Agreement”), we granted Novartis an exclusive, worldwide, royalty-bearing license to gevokizumab (“VPM087”) (an early clinical stage product candidate) and related know-how and patents. Under the terms of the XOMA-052 License Agreement, Novartis will be solely responsible for the development and commercialization of VPM087 and products containing such antibody.

2

Under the XOMA-052 License Agreement, we received total consideration of $30.0 million in 2017 for the license and rights granted to Novartis. Of the total consideration, $15.7 million was paid in cash and $14.3 million (equal to €12.0 million) was paid by Novartis Institutes for Biomedical Research, Inc. (“NIBR”), on our behalf, to settle our loan with Les Laboratories Servier (“Servier”). In addition, NIBR extended the maturity date on our debt to Novartis to September 30, 2022. We also received $5.0 million related to the sale of 539,131 shares of our common stock, at a price per share of $9.2742. Based on the achievement of pre-specified criteria, we are eligible to receive up to $438.0 million in development, regulatory and commercial milestones. We are also eligible to receive royalties on sales of licensed products, which are tiered based on sales levels and range from a high single digit percentage rate to a low double-digit percentage rate. This program is in early clinical testing.

Under the second license agreement (the “IL-1 Target License Agreement”), we granted Novartis non-exclusive licenses to our intellectual property covering the use of IL-1 beta targeting antibodies in the treatment and prevention of cardiovascular disease and other diseases and conditions, and an option to obtain an exclusive license (the “Exclusivity Option”) to such intellectual property for the treatment and prevention of cardiovascular disease. We also granted Novartis the right of first negotiation with respect to certain transactions relating to the licensed intellectual property.

Under the IL-1 Target License Agreement, we received an upfront cash payment of $10.0 million. In addition, we are eligible to receive low single-digit royalties on canakinumab sales in cardiovascular indications.

In October 2018, Novartis disclosed that it received a Complete Response Letter (“CRL”) from the Food and Drug Administration (“FDA”) regarding the supplemental Biologics License Application for cardiovascular risk reduction related to canakinumab. In December 2018, Novartis withdrew the European marketing application for canakinumab for cardiovascular risk reduction.

Unless terminated earlier, the XOMA-052 License Agreement and IL-1 Target License Agreement will remain in effect, on a country-by-country and product-by-product basis, until Novartis’ royalty obligations end. The two agreements contain customary termination rights relating to material breach by either party. Novartis also has a unilateral right to terminate the XOMA-052 License Agreement on a product-by-product and country-by-country basis or in its entirety on six months’ prior written notice. Under the IL-1 Target License Agreement, Novartis has a unilateral right to terminate the agreement on a product-by-product and country-by-country basis or in its entirety upon a prior written notice.

Novartis – Anti-TGFβ Antibody

In September 2015, we and Novartis International Pharmaceutical Ltd. (“Novartis International”) entered into a license agreement (the “License Agreement”) under which we granted Novartis International an exclusive, worldwide, royalty-bearing license to our anti-TGF-β antibody program (“NIS793”). Novartis International is solely responsible for the development and commercialization of the antibodies and products containing the antibodies arising from this program.

Under the License Agreement, we received a $37.0 million upfront fee, and are eligible to receive up to a total of $480.0 million in development, regulatory and commercial milestones. We also are eligible to receive royalties on sales of licensed products, which are tiered based on sales levels and range from a mid-single digit percentage rate to a low double-digit percentage rate. This program is currently in early clinical testing.

Rezolute

On December 6, 2017, we entered into a license agreement with Rezolute, Inc. (formerly AntriaBio, Inc.) (“Rezolute”) pursuant to which we granted an exclusive global license to Rezolute to develop and commercialize X358 (now RZ358), a Phase 2 product candidate, for all indications. We and Rezolute also entered into a common stock purchase agreement.

Under the terms of the license agreement, Rezolute is responsible for all development, regulatory, manufacturing and commercialization activities associated with RZ358 and is required to make certain clinical, regulatory and annual net sales milestone payments to us of up to $232.0 million in the aggregate based on the achievement of pre-specified criteria. Rezolute is also obligated to pay us royalties ranging from the high single digits to the mid-teens based upon annual net sales of RZ358. Rezolute is obligated to take customary steps to advance RZ358, including using diligent efforts to commence the next clinical study for RZ358 by a certain deadline and to meet certain spending requirements on an annual basis for the program until a marketing approval application for RZ358 is accepted by the FDA. Rezolute’s obligation to pay royalties with respect to a particular RZ358 product and country will continue for the longer of the date of expiration of the last valid patent claim covering the product in that country, or twelve years from the date of the first commercial sale of the product in that country.

3

Under the terms of the license agreement, Rezolute is required to pay us a low single-digit royalty on sales of Rezolute’s other products from its existing programs, currently in preclinical and early clinical stages. Rezolute’s obligation to pay royalties with respect to a particular Rezolute product and country will continue for the longer of twelve years from the date of the first commercial sale of the product in that country or for so long as Rezolute or its licensee is selling such product in such country, provided that such royalty will terminate upon the termination of the licensee’s obligation to make payments to Rezolute based on sales of such product in such country.

We also granted Rezolute an option through June 1, 2019 for an exclusive license for their choice of one of our preclinical insulin receptor monoclonal antibody fragments, including X129. If Rezolute exercises the option, we will be eligible for an upfront option fee and additional clinical, regulatory and annual net sales milestone payments to us of up to $237.0 million in the aggregate based on the achievement of pre-specified criteria as well as royalties ranging from a high single digit percentage rate to a low double-digit percentage rate based on annual net sales. The license agreement contains customary termination rights relating to material breach by either party. Rezolute also has a unilateral right to terminate the license agreement in its entirety on ninety-days’ notice at any time. We have the right to terminate the license agreement if Rezolute challenges the licensed patents.

In March 2018, we and Rezolute amended the license agreement and common stock purchase agreement. Pursuant to the as-amended terms of the license agreement and common stock purchase agreement, Rezolute is required to pay us $6.0 million in cash, to issue us $8.5 million worth of its common stock, and to issue us 7,000,000 shares of its common stock, contingent on the completion of its financing activities. Further, in the event that Rezolute does not complete a financing that raises at least $20.0 million in aggregate gross proceeds (“Qualified Financing”) by March 31, 2019 (the “2019 Closing”), it shall issue to us an additional number of shares of its common stock equal to $8.5 million divided by the weighted average of the closing bid and ask prices or the average closing prices of Rezolute’s common stock on the ten-day trading period prior to March 31, 2019. Finally, if Rezolute is unable to complete a Qualified Financing by March 31, 2020, it will be obliged to pay us $15.0 million in order to maintain the license. Under the common stock purchase agreement, Rezolute granted us the right and option to sell the greater of (i) 5,000,000 shares of common stock or (ii) one third of the aggregate shares held by us upon failure by Rezolute to list its shares of its common stock on the Nasdaq Stock Market or a similar national exchange on or prior to December 31, 2018.

During the year ended December 31, 2018, Rezolute closed a debt financing activity for gross proceeds of $4.0 million, which triggered the Initial Closing, and completed an Interim Financing Closing, as defined in the common stock purchase agreement. These financing activities resulted in receipt of 8,093,010 shares of Rezolute’s common stock and cash of $0.5 million. Under the amended license agreement, we are also entitled to receive $0.3 million of reimbursable technology transfer expenses from Rezolute. On January 7, 2019, we and Rezolute further amended the license agreement and common stock purchase agreement. The license agreement was amended to eliminate the requirement that equity securities be issued to us upon the closing of the Qualified Financing (as defined in the license agreement) and to replace it with a requirement that Rezolute: (1) make five cash payments to us totaling $8.5 million following the closing of a Qualified Financing on or before specified staggered future dates through September 2020 (the “Future Cash Payments”); and (2) provide for early payment of the Future Cash Payments (only until the above referenced $8.5 million is reached) by making cash payments to us equal to 15% of the net proceeds of each future financing following the closing of the Qualified Financing, with such payments to be credited against any remaining unpaid Future Cash Payments in reverse order of their future payment date. In accordance with the terms of the license agreement, we received additional $5.5 million in cash upon the closing of the Qualified Financing.

In addition, the license agreement amendment revised the amount Rezolute is required to expend on development of RZ358 and related licensed products and revised provisions with respect to Rezolute’s diligence efforts in conducting clinical studies. Lastly, the common stock purchase agreement was amended to remove certain provisions related to the issuance of equity to us in accordance with the new provisions regarding the Future Cash Payments in the license agreement. Specifically, the common stock purchase agreement was amended to provide XOMA the right to sell up to 5,000,000 shares of Rezolute common stock currently held by us, back to Rezolute if it fails to list its shares of common stock on the Nasdaq Stock Market or a similar national exchange on or prior to December 31, 2019. Only 2,500,000 shares may be sold back to Rezolute during calendar year 2020. Any such shares may be sold back to Rezolute at the average of the closing bid and asked prices of its common stock quoted on its principal trading market on the date of such put option exercise.

Takeda

In November 2006, we entered into a collaboration agreement with Takeda under which we agreed to discover and optimize therapeutic antibodies against multiple targets selected by Takeda.

Under the terms of this agreement, we may receive additional milestone payments aggregating up to $19.0 million relating to one undisclosed product candidate and low single-digit royalties on future sales of all products subject to this license. Our right to milestone payments expires on the later of the receipt of payment from Takeda of the last amount to be paid under the agreement or the cessation by Takeda of all research and development activities with respect to all program antibodies, collaboration targets or

4

collaboration products. Our right to royalties expires on the later of 13.5 years from the first commercial sale of each royalty-bearing discovery product or the expiration of the last-to-expire licensed patent.

In February 2009, we expanded our existing collaboration to provide Takeda with access to multiple antibody technologies, including a suite of research and development technologies and integrated information and data management systems. We may receive milestones of up to $3.3 million per discovery product candidate and low single-digit royalties on future sales of all antibody products subject to this license. Our right to milestone payments expires on the later of the receipt of payment from Takeda of the last amount to be paid under the agreement or the cessation by Takeda of all research and development activities with respect to all program antibodies, collaboration targets or collaboration products. Our right to royalties expires on the later of 10 years from the first commercial sale of such royalty-bearing discovery product or the expiration of the last-to-expire licensed patent.

Ology Bioservices

On November 4, 2015, we entered into an asset purchase agreement with Ology Bioservices, Inc. (“Ology Bioservices”) (formerly Nanotherapeutics Inc.) (the “Ology Bioservices Purchase Agreement”), under which Ology Bioservices agreed to acquire our biodefense business and related assets. Under the terms of this agreement, we are eligible to receive a 15% royalty on net sales of any future Ology Bioservices products covered by or involving the related patents or know-how. Further details of the Ology Bioservices Purchase Agreement are provided in the section below, “Sale of Biodefense Assets and Manufacturing Facility.”

Acquisitions

Agenus Royalty Purchase Agreement

On September 20, 2018, we entered into a Royalty Purchase Agreement (the “Royalty Purchase Agreement”) with Agenus. Under the Royalty Purchase Agreement, we purchased from Agenus the right to receive 33% of the future royalties due to Agenus from Incyte (net of certain royalties payable by Agenus to a third party) and 10% of all future developmental, regulatory and sales milestones on sales of six Incyte immuno-oncology assets, with the exception of an expected near-term milestone associated with the entry of INCAGN2390 (anti-TIM-3) into the clinical trial. In addition, we purchased from Agenus the right to receive 33% of the future royalties due to Agenus from Merck and 10% of all future developmental, regulatory and sales milestones on sales of an undisclosed Merck immuno-oncology product currently in clinical development. Pursuant to the Royalty Purchase Agreement, our share in future potential development, regulatory and commercial milestones is up to $59.5 million and the royalties have no limit. Under the terms of the Royalty Purchase Agreement, we paid Agenus $15.0 million. We have financed $7.5 million of the purchase price with a three-year term loan under our Loan and Security Agreement with Silicon Valley Bank (“SVB”) dated May 7, 2018.

Proprietary Product Candidates

We have a pipeline of unique monoclonal antibodies and technologies that we intend to attempt to license to pharmaceutical and biotechnology companies to further their clinical development. A summary of these product candidates is provided below:

|

|

• |

X213 (formerly LFA 102) is a first-in-class allosteric inhibitor of prolactin action. It is a humanized IgG1-Kappa monoclonal antibody that binds to the extracellular domain of the human prolactin receptor with high affinity at an allosteric site. The antibody has been shown to inhibit prolactin-mediated signaling, and it is potent and similarly active against several animal and human prolactin receptors. |

|

|

• |

XMetA is an insulin receptor-activating antibody designed to provide long-acting reduction of hyperglycemia in Type 2 diabetic patients, potentially reducing the advancement to a number of insulin injections needed to control their blood glucose levels. |

|

|

• |

IL-2 targets interleukin 2 and has long been recognized as an effective therapy for metastatic melanoma and renal cell carcinoma, but it has serious dose-limiting toxicities that prevent broad clinical use. We have generated novel antibodies that, when given with IL-2, are intended to steer IL-2 to enhance its positive impact with less toxicity, potentially improving the therapeutic index over standard IL-2 therapy. |

|

|

• |

PTH1R is an anti-parathyroid receptor pipeline that includes several unique functional antibody antagonists targeting PTH1R, a G-protein-coupled receptor involved in the regulation of calcium metabolism. These antibodies have shown promising efficacy in in vivo studies and could potentially address unmet medical needs, including primary hyperparathyroidism and humoral hypercalcemia of malignancy (“HHM”). HHM is present in many advanced cancers and is caused by high serum calcium due to increased levels of the PTH1R ligand PTH-related peptide (“PTHrP”). Current HHM treatments often fall short and many cancer patients die from ‘metabolic death'. Our PTH1R antibodies could be beneficial for the treatment of HHM. |

5

Technologies Available for Non-Exclusive License

We have a unique set of antibody discovery, optimization and development technologies available for licensing, including:

|

|

• |

ADAPT™ (Antibody Discovery Advanced Platform Technologies): proprietary human antibody phage display libraries, integrated with yeast and mammalian display, which can be integrated into antibody discovery programs through license agreements. We believe access to ADAPT™ Integrated Display offers a number of benefits because it enables the diversity of phage libraries to be combined with accelerated discovery due to rapid immunoglobulin (“IgG”) reformatting and fluorescence-activated cell sorting based screening using yeast and mammalian display. This increases the probability of success in finding rare and unique functional antibodies directed to targets of interest. |

|

|

• |

ModulX™: technology which allows modulation of biological pathways using monoclonal antibodies and offers insights into regulation of signaling pathways, homeostatic control, and disease biology. Using ModulX™, we have generated product candidates with novel mechanisms of action that specifically alter the kinetics of interaction between molecular constituents (e.g. receptor-ligand). ModulX™ technology enables expanded target and therapeutic options and offers a unique approach in the treatment of disease. |

|

|

• |

OptimX™ technologies: |

|

|

• |

Human Engineering™ (“HE™”): a proprietary humanization technology that allows modification of non-human monoclonal antibodies to reduce or eliminate detectable immunogenicity and make them suitable for medical purposes in humans. The technology uses a unique method developed by us, based on analysis of the conserved structure-function relationships among antibodies. The method defines which residues in a non-human variable region are candidates to be modified. The result is an HE™ antibody with preserved antigen binding, structure and function that has eliminated or greatly reduced immunogenicity. HE™ technology was used in development of gevokizumab (VPM087) and certain other antibody products. |

|

|

• |

Targeted Affinity Enhancement™ (“TAE™”): a proprietary technology involving the assessment and guided substitution of amino acids in antibody variable regions, enabling efficient optimization of antibody binding affinity and selectivity. TAE™ generates a comprehensive map of the effects of amino acid mutations in the complementarity-determining region likely to impact binding. The technology has been licensed to a number of companies. |

Sale of Biodefense Assets and Manufacturing Facility

Ology Bioservices

On November 4, 2015, we entered the Ology Bioservices Purchase Agreement with Ology Bioservices, under which Ology Bioservices agreed to acquire our biodefense business and related assets (including certain contracts with the U.S. government), and to assume certain liabilities of XOMA. As part of that transaction, the parties, subject to the satisfaction of certain conditions, entered into an intellectual property license agreement (the “Ology Bioservices License Agreement”), under which we agreed to license to Ology Bioservices certain intellectual property rights related to the purchased assets. Under the Ology Bioservices License Agreement, we were eligible for up to $4.5 million of cash payments and 23,008 shares of common stock of Ology Bioservices, based upon Ology Bioservices achieving certain specified future operational objectives. In addition, we are eligible to receive a 15% royalty on net sales of any future Ology Bioservices products covered by or involving the related patents or know-how. Our right to royalties continues until the expiration of the last-to-expire licensed patent.

In February 2017, we executed an Amendment and Restatement to both the Ology Bioservices Purchase Agreement and Ology Bioservices License Agreement primarily to (i) remove the obligation to issue 23,008 shares of common stock of Ology Bioservices under the Ology Bioservices Purchase Agreement, and (ii) revise the payment schedule related to the timing of the $4.5 million cash payments due to us under the Ology Bioservices License Agreement. Of the $4.5 million, $3.0 million was contingent upon Ology Bioservices achieving certain specified future operating objectives. In the first quarter of 2017, we were entitled to receive $1.6 million under the agreement that was received in quarterly payments through September 2018. In the third quarter of 2017, Ology Bioservices achieved the specified operating objectives and we earned the $3.0 million milestone fee that was received in monthly payments through July 2018. Of the total $4.6 million owed to us, we received $2.4 million during the year ended December 31, 2018, and $2.2 million during the year ended December 31, 2017, which was recognized as other income in our consolidated statement of operations and comprehensive (loss) income. No further payments remain under the agreement, but we are still eligible to receive royalties in the future.

6

Sale of Future Revenue Streams

Royalty Acquisition Agreements

On December 21, 2016, we entered into two Royalty Interest Acquisition Agreements (together, the “Royalty Acquisition Agreements”) with HealthCare Royalty Partners II, L.P. (“HCRP”). Under the first Royalty Acquisition Agreement, we sold our right to receive milestone payments and royalties on future sales of products subject to a license agreement, dated August 18, 2005, between XOMA and Pfizer, Inc. (“Pfizer”) (formerly Wyeth) for an upfront cash payment of $6.5 million, plus potential additional payments totaling $4.0 million in the event three specified net sales milestones are met by Pfizer in 2017, 2018 and 2019. The 2017 sales milestone was not achieved. Based on estimated sales for 2018, the 2018 sales milestone was not achieved. We remain eligible to receive up to $2.0 million if specified net sales milestones are achieved in 2019. Under the second Royalty Acquisition Agreement entered into in December 2016, we sold all rights to royalties under an Amended and Restated License Agreement dated October 27, 2006 between XOMA and Shire Plc. (formerly Dyax, Corp.) for a cash payment of $11.5 million.

Debt Agreements

Novartis

In connection with the collaboration between XOMA and Novartis AG (then Chiron Corporation), a secured note agreement was executed in May 2005. The note agreement is secured by our interest in the collaboration and was due and payable in full on June 21, 2015. On June 19, 2015, we and NVDI, who assumed the note agreement, agreed to extend the maturity date of our secured note agreement from June 21, 2015 to September 30, 2015, which was then subsequently extended to September 30, 2020. On September 22, 2017, in connection with the XOMA-052 License Agreement with Novartis, we and NIBR, who assumed the note agreement from NVDI, executed an amendment to the note agreement under which we further extended the maturity date of the note to September 30, 2022. At December 31, 2018, the outstanding principal balance under this note agreement totaled $15.2 million.

Silicon Valley Bank Loan Agreement

In May 2018, we executed a Loan and Security Agreement (the “Loan Agreement”) with SVB. Under the Loan Agreement, upon our request, SVB may make advances available to us of up to $20.0 million. We may borrow advances under the Term Loan from May 7, 2018 (the “Effective Date”) until the earlier of March 31, 2020 or an event of default. The interest rate will be calculated at a rate equal to the greater of (i) 4.75%, and (ii) 0.25% plus the prime rate as reported from time to time in The Wall Street Journal.

In connection with the Loan Agreement, we issued a warrant to SVB which is exercisable in whole or in part for up to an aggregate of 6,332 shares of common stock with an exercise price of $23.69 per share (the “Warrant”). The Warrant may be exercised on a cashless basis and is exercisable within 10 years from the date of issuance or upon the consummation of certain acquisitions of XOMA.

In September 2018, we borrowed $7.5 million under the Loan Agreement in connection with the Agenus royalty purchase agreement.

In March 2019, we issued a second warrant to SVB which is exercisable in whole or in part for up to an aggregate of 4,845 shares of common stock with an exercise price of $14.71 per share. The new warrant may be exercised on a cashless basis and is exercisable within 10 years from the date of issuance or upon the consummation of certain acquisitions of XOMA.

Servier

In December 2010, in connection with the collaboration agreement entered into with Servier, we executed a loan agreement with Servier (the “Servier Loan Agreement”), which provided for an advance of up to €15.0 million (or $19.5 million at the exchange rate on the date of funding). The loan was secured by an interest in XOMA’s intellectual property rights to all gevokizumab (VPM087) indications worldwide, excluding certain rights in the United States and Japan.

On August 25, 2017, NIBR settled the Servier Loan Agreement in cash by paying directly to Servier $14.3 million, which represented the outstanding balance of the loan based on a euro to dollar exchange rate of 1.1932. The funds that NIBR paid directly to Servier were a portion of the upfront payment due to us under the XOMA-052 License Agreement. As a result of the debt being fully paid, the intellectual property securing the Servier Loan Agreement was released.

7

Hercules Loan and Security Agreement

In February 2015, we entered into a Loan and Security Agreement with Hercules Technology Growth Capital, Inc., (the “Hercules Loan Agreement”) under which we borrowed $20.0 million.

On March 21, 2017, the Hercules Term Loan was paid in full and we were not required to pay the 1% prepayment charge due pursuant to the terms of the loan.

Research and Development

Our research and development expenses include costs of personnel, supplies, facilities and equipment, consultants, third-party costs and other expenses related to preclinical and clinical testing.

Prior to 2017, our research and development activities can be divided into those related to our internal projects and those related to collaborative and contract arrangements, which are reimbursed by our collaborators. In March 2017, we initiated a corporate reorganization to discontinue internal product development and terminated our clinical programs as of June 30, 2017, both of which significantly reduced our research and development expenses.

Competition

The biotechnology and pharmaceutical industries are subject to continuous and substantial technological change. Some of the drugs our licensees are developing may compete with existing therapies or other drugs in development by other companies. Furthermore, academic institutions, government agencies and other public and private organizations conducting research may seek patent protection with respect to potentially competing products or technologies and may establish collaborative arrangements with our competitors. There can be no assurance that developments by others will not render our, or our licensees’, products or technologies obsolete or uncompetitive.

Additionally, our recently-undertaken royalty aggregator model faces competition on at least two fronts. First, there are other companies, funds and other investment vehicles seeking to aggregate royalties or provide alternative financing to development-stage biotechnology and pharmaceutical companies. The competitive companies, funds and other investment vehicles may have a lower target rate of return, a lower cost of capital or access to greater amounts of capital and thereby may be able to acquire assets that we are also targeting for acquisitions. Second, existing or potential competitors to our partners’ and licensees’ products, particularly large pharmaceutical companies, may have greater financial, technical and human resources than our licensees. Accordingly, these competitors may be better equipped to develop, manufacture and market products. Many of these companies also have extensive experience in preclinical testing and human clinical trials, obtaining FDA and other regulatory approvals and manufacturing and marketing pharmaceutical products.

For a discussion of the risks associated with competition, see below under “Item 1A. Risk Factors.”

Government Regulation

The research and development, manufacturing and marketing of pharmaceutical products are subject to regulation by numerous governmental authorities in the United States and other countries. We and our partners and licensees, depending on specific activities performed, are subject to these regulations. In the United States, pharmaceuticals are subject to regulation by both federal and various state authorities, including the FDA. The Federal Food, Drug and Cosmetic Act and the Public Health Service Act govern the testing, manufacture, safety, efficacy, labeling, storage, record keeping, approval, advertising and promotion of pharmaceutical products and there are often comparable regulations that apply at the state level. There are similar regulations in other countries as well. For both currently marketed and products in development, failure to comply with applicable regulatory requirements can, among other things, result in delays, the suspension of regulatory approvals, as well as possible civil and criminal sanctions. In addition, changes in existing regulations could have a material adverse effect on us or our partners.

For a discussion of the risks associated with government regulations, see below under “Item 1A. Risk Factors.”

8

Intellectual Property

Intellectual property is important to our business and our future income streams will depend in part on our ability to obtain issued patents, and our partners’ and licensees’ ability to operate without infringing on the proprietary rights of others. We hold and have filed applications for a number of patents in the United States and internationally to protect our products and technology. We also have obtained or have the right to obtain licenses to, or income streams based on, certain patents and applications filed by others. However, the patent position of biotechnology companies generally is highly uncertain and consistent policy regarding the breadth of allowed claims has not emerged from the actions of the U.S. Patent and Trademark Office with respect to biotechnology patents. Accordingly, no assurance can be given that our, or our partners’ or licensees’ patents will afford protection against competitors with similar products or others will not obtain patents claiming aspects similar to those covered by our, or our partners’ or licensees’ patent applications. Below is a list of our patents and patent applications related to our programs:

|

Licensee/Partner |

Program |

Representative Patents/Applications |

Subject matter |

Expected expiry |

|

Novartis |

Anti-IL-1b |

US 7,531,166 US 7,582,742 EP 1 899 378

US 7,695,718 US 8,101,166 US 8,586,036 US 9,163,082

US 8,637,029

JP 5763625 |

Gevokizumab and other antibodies and antibody fragments with similar binding properties for IL-1β

Methods of treating Type 2 diabetes or Type 2 diabetes-induced diseases or conditions with high affinity antibodies and antibody fragments that bind to IL-1β

Methods of treating gout with certain doses of IL-1β binding antibodies or binding fragments

Pharmaceutical compositions comprising anti-IL-1β binding antibodies or fragments for reducing acute coronary syndrome in a subject with a history of myocardial infarction. |

2027

2027

2028

2030 |

|

Novartis |

Anti-TGFb |

US 8,569,464 US 9,145,458 US 9,714,285

US 10,167,334 |

TGFβ antibodies and methods of use thereof

Combination therapy using an inhibitor of TGFb and an inhibitor of PD-1 for treating or preventing recurrence of cancer |

2032

2036 |

|

Novartis |

Anti-CD40 |

US 8,828,396* |

Silent Fc variants of anti-CD40 antibodies |

2031 |

|

Rezolute |

Anti-INSR |

US 9,944,698 EP 2 480 254 JP 5849050

WO2016/141111 |

Insulin receptor-modulating antibodies having the functional properties of RZ358

Methods of treating or preventing post-prandial hypoglycemia after gastric bypass surgery using a negative modulator antibody to the insulin receptor |

2030

2036 |

9

|

Ology Bio |

Anti-BoNT |

US 8,821,879 EP 2 473 191 |

Coformulations of anti- botulinum neurotoxin antibodies |

2030 |

|

PrlA Pharma |

Anti-PRLR |

US 7,867,493 EP 2 059 535 |

Prolactin receptor antibodies |

2027 |

|

Various |

Bacterial cell expression/ Phage display libraries |

US 8,546,307 EP 2 344 686 US 7,094,579 EP 2 060 628 |

XOMA phage display library components |

2022 |

|

Actively seeking out license |

Anti-PTH1R |

WO2018/026748 |

Parathyroid Hormone Receptor 1 Antibodies and Uses Thereof |

2037 |

|

Actively seeking out license |

Anti-IL2 |

WO2018/064255** |

Interleukin-2 Antibodies and Uses Thereof |

2037 |

* Novartis-owned patent

**Jointly-owned with Medical University of South Carolina Foundation for Research Development

If certain patents issued to others are upheld or if certain patent applications filed by others are issued and upheld, our partners and licensees may require certain licenses from others to develop and commercialize certain potential products incorporating our technology. There can be no assurance that such licenses, if required, will be available on acceptable terms.

We protect our proprietary information, in part, by confidentiality agreements with our employees, consultants and partners. These parties may breach these agreements, and we may not have adequate remedies for any breach. To the extent that we or our consultants or partners use intellectual property owned by others, we may have disputes with our consultants or partners or other third parties, as to the rights in related or resulting know-how and inventions.

Our business model is dependent on third parties achieving specified development milestones and product sales. Our pipeline currently includes over 40 fully-funded programs from which we could potentially receive royalties if the programs achieve marketability. Novartis is developing several of the programs in our pipeline. While we do not expect the discontinuation of any one program would have a material impact on our business, the discontinuation of all programs by Novartis could have a material effect on our business and financial condition.

Organization

We were incorporated in Delaware in 1981 and became a Bermuda-exempted company in December 1998. Effective December 31, 2011, we changed our jurisdiction of incorporation from Bermuda to Delaware and changed our name from XOMA Ltd. to XOMA Corporation. When referring to a time or period before December 31, 1998 or after December 31, 2011, the terms “Company” and “XOMA” refer to XOMA Corporation, a Delaware corporation; when referring to a time or period between December 31, 1998 and December 31, 2011, such terms refer to XOMA Ltd., a Bermuda company.

Our principal executive offices are located at 2200 Powell Street, Suite 310, Emeryville, California 94608, and we maintain a registered office located at Corporation Trust Center, 1209 Orange Street, Wilmington, Delaware 19801. Our telephone number at our principal executive offices is (510) 204-7200. Our website address is www.xoma.com. The information found on our website is not part of this or any other report filed with or furnished to the Securities and Exchange Commission (“SEC”).

10

Employees

As of March 4, 2019, we employed 11 full-time employees. None of our employees are unionized. Our employees are primarily engaged in executive, business development, legal, finance and administrative positions.

Available Information

The following information can be found on our website at http://www.xoma.com or can be obtained free of charge by contacting our Investor Relations Department at investorrelations@xoma.com or by calling (510) 204-7482:

|

|

• |

Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to those reports filed or furnished under Section 13(a) or 15(d) of the Exchange Act will be available as soon as reasonably practicable after such material is electronically filed with the SEC. |

|

|

• |

Our policies related to corporate governance, including our Code of Ethics applying to our directors, officers and employees (including our principal executive officer and principal financial and accounting officer) that we have adopted to meet the requirements set forth in the rules and regulations of the SEC and its corporate governance principles. |

|

|

• |

The charters of the Audit, Compensation and Nominating & Governance Committees of our Board of Directors. |

We intend to satisfy the applicable disclosure requirements regarding amendments to, or waivers from, provisions of our Code of Ethics by posting such information on our website.

11

The following risk factors and other information included in this annual report should be carefully considered. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties not presently known to us also may impair our business operations. If any of the following risks occur, our business, financial condition, operating results and cash flows could be materially adversely affected.

Risks Related to our Royalty Aggregator Strategy

Our acquisitions of potential future royalty and/or milestone payments may not produce anticipated revenues and/or may be negatively affected by a default or bankruptcy of the licensor(s) or licensee(s) under the applicable license agreement(s) covering such potential royalties and/or milestones, and if such transactions are secured by collateral, we may be, or may become, under-secured by the collateral or such collateral may lose value and we will not be able to recuperate our capital expenditures associated with the acquisition.

We are engaged in a continual review of opportunities to acquire royalties and other intellectual property assets as part of our royalty aggregator strategy or to acquire companies that hold royalty assets. Generally, at any time, we seek to have acquisition opportunities in various stages of active review, including, for example, our engagement of consultants and advisors to analyze particular opportunities, technical, financial and other confidential information, submission of indications of interest and involvement as a bidder in competitive auctions. Many potential acquisition targets do not meet our criteria, and for those that do, we may face significant competition for these acquisitions from other royalty buyers and enterprises. Competition for future asset acquisition opportunities in our markets could increase the price we pay for such assets and could reduce the number of potential acquisition targets. The success of our acquisitions is based on our ability to make accurate assumptions regarding the valuation, timing and amount of future royalty and milestone payments as well as the viability of the underlying technology. The failure of any of these acquisitions to produce anticipated revenues may materially and adversely affect our financial condition and results of operations.

Some of these acquisitions may expose us to credit risk in the event of a default by or bankruptcy of the licensor(s) or licensee(s) that are parties the applicable license agreement(s) covering the potential milestone and royalty streams being acquired. While we generally try to structure our potential receipt of milestone and royalty payments to minimize the risk associated with such a default or bankruptcy, there can be no assurance that any such default or bankruptcy will not adversely affect our ability to receive future potential royalty and/or milestone payments. To mitigate this risk, on occasion, we may obtain a security interest as collateral in the assets of such counterparty. Our credit risk in respect of such counterparty may be exacerbated when the collateral held by us cannot be realized upon or is liquidated at prices not sufficient to recover the full amount we are due pursuant to the terms of the particular assets. This could occur in circumstances where the original collateral was not sufficient to cover a complete loss (e.g., our interests were only partially secured) or may result from the deterioration in value of the collateral, so that, in either such case, we are unable to recuperate our full capital outlay. Any such losses resulting therefrom could materially and adversely affect our financial condition and results of operations.

Many of our potential royalty acquisitions may be associated with drug products that are in clinical development and have not yet been commercialized. To the extent that such products are not successfully developed and commercialized, our financial condition and results of operations may be negatively impacted.

As part of our royalty aggregator strategy, we will likely purchase future milestone and royalty streams associated with drug products which are in clinical development and have not yet been commercialized. To the extent that any such drug products are not successfully developed and subsequently commercialized, the value of our acquired potential milestone and royalty streams will be negatively affected. The ultimate success of our royalty aggregator strategy will depend on our ability to properly identify and acquire high quality products and the ability of the applicable counterparty to innovate, develop and commercialize their products, in increasingly competitive and highly regulated markets. Their inability to do so would negatively affect our ability to receive royalty payments. In addition, we are dependent, to a large extent, on third parties to enforce certain rights for our benefit, such as protection of a patent estate, adequate reporting and other protections, and their failure to do so would negatively impact our financial condition and results of operation.

12

We depend on our licensees and royalty-agreement counterparties for the determination of royalty and milestone payments. While we typically have primary or back-up rights to audit our licensees and royalty-agreement counterparties, the independent auditors may have difficulty determining the correct royalty calculation, we may not be able to detect errors and payment calculations may call for retroactive adjustments. We may have to exercise legal remedies, if available, to resolve any disputes resulting from the audit.

The royalty and milestone payments we may receive are dependent on our licensees based on their reported achievement of regulatory and developmental milestones and product sales. Each licensee's calculation of the royalty payments is subject to and dependent upon the adequacy and accuracy of its sales and accounting functions, and errors may occur from time to time in the calculations made by a licensee and/or a licensee may fail to report the achievement of royalties or milestones in whole or in part. Our license and royalty agreements typically provide us the primary or back-up right to audit the calculations and sales data for the associated royalty payments; however, such audits may occur many months following our recognition of the royalty revenue, may require us to adjust our royalty revenues in later periods and may require expense on the part of the Company. Further, our licensees and royalty-agreement counterparties may be uncooperative or have insufficient records, which may complicate and delay the audit process.

Although we intend to regularly exercise our royalty audit rights as necessary and to the extent available, we rely in the first instance on our licensees and royalty-agreement counterparties to accurately report the achievement of milestones and royalty sales and calculate and pay applicable milestones and royalties and, upon exercise of such royalty and other audit rights, we rely on licensees' and royalty-agreement counterparties' cooperation in performing such audits. In the absence of such cooperation, we may be forced to exercise legal remedies, if available, to enforce our agreements.

The lack of liquidity of our intellectual property acquisitions may adversely affect our business and, if we need to sell any of our acquired assets, we may not be able to do so at a favorable price, if at all. As a result, we may suffer losses.

We generally acquire patents, milestone and royalty rights that have limited secondary resale markets and may be subject to transfer restrictions. The illiquidity of most of our intellectual property related assets may make it difficult for us to dispose of them at a favorable price if at all and, as a result, we may suffer losses if we are required to dispose of any or all such assets in a liquidation or otherwise. In addition, if we liquidate all or a portion of our purchased royalty stream assets quickly or relating to a liquidation, we may realize significantly less than the value at which we had previously recorded these assets.

Our royalty aggregator strategy may require that we register with the SEC as an “investment company” in accordance with the Investment Company Act of 1940.

In 2017 we began transforming our business model from a traditional biotech enterprise discovering and developing innovative therapeutics from our own platform of antibody technologies to a royalty aggregator where we focus on expanding our pipeline of fully-funded programs by acquiring potential milestone and royalty revenue streams on additional product candidates from third parties and out-licensing our internally developed product candidates.

The rules and interpretations of the SEC and the courts, relating to the definition of "investment company" are very complex. While we currently intend to conduct our operations so that we will not be an investment company under applicable SEC interpretations, we can provide no assurance that the SEC would not take the position that the Company would be required to register under the Investment Company Act of 1940(the “‘40 Act”) and comply with the ‘40 Act’s registration and reporting requirements, capital structure requirements, affiliate transaction restrictions, conflict of interest rules, requirements for disinterested directors, and other substantive provisions. We monitor our assets and income for compliance under the ‘40 Act and seek to conduct our business activities to ensure that we do not fall within its definitions of “investment company” or qualify under one of the exemptions or exclusions provided by the ‘40 Act. If we were to become an “investment company” and be subject to the restrictions of the ‘40 Act, those restrictions would likely require changes in the way we do business and add significant administrative burdens to our operations. To ensure that we do not fall within the ‘40 Act, we may need to take various actions which we might otherwise not pursue. These actions may include restructuring the Company and/or modifying our mixture of assets and income.

13

Risks Related to our Financial Results and Capital Requirements

We have sustained losses in the past, and we expect to sustain losses in the foreseeable future.

With the exception of the year ended December 31, 2017, we have incurred significant operating losses and negative cash flows from operations since our inception. We had a net loss of $13.3 million for the year ended December 31, 2018 and net income of $14.6 million for the year ended December 31, 2017. As of December 31, 2018, we had an accumulated deficit of $1.2 billion. We do not know whether we will ever achieve sustained profitability or whether cash flow from future operations will be sufficient to meet our needs.

To date, we have financed our operations primarily through the sale of equity securities and debt, and collaboration and licensing arrangements. The size of our future net losses will depend, in part, on the rate of our future expenditures and our and our partners’ ability to generate revenues. If our partners’ product candidates are not successfully developed or commercialized by our licensees, or if revenues are insufficient following regulatory approval, we will not achieve profitability and our business may fail. Our ability to achieve profitability is dependent in large part on the success of our and our licensees’ ability to license product candidates, and the success of our licensees’ development programs, both of which are uncertain. Our success is also dependent on our licensees obtaining regulatory approval to market product candidates which may not materialize or prove to be successful.

Our new strategy may require us to raise additional funds to acquire royalty assets; we cannot be certain that funds will be available or available at an acceptable cost of capital, and if they are not available, we may be unsuccessful in acquiring royalty assets to sustain the business in the future.

We may need to commit substantial funds to continue our business, and we may not be able to obtain sufficient funds on acceptable terms, if at all. Any additional debt financing or additional equity that we raise may contain terms that are not favorable to us and/or result in dilution to our stockholders, including pursuant to our 2018 ATM Agreement. If we raise additional funds through licensing arrangements with third parties, we may be required to relinquish some rights to our technologies or our product candidates, grant licenses on terms that are not favorable to us or enter into a license arrangement for a product candidate at an earlier stage of development or for a lesser amount than we might otherwise choose.

If adequate funds are not available on a timely basis, we may:

|

|

• |

reduce or eliminate royalty aggregation efforts; or |

|

|

• |

further reduce our capital or operating expenditures; or |

|

|

• |

curtail our spending on protecting our intellectual property. |

We have significantly restructured our business and revised our business plan and there are no assurances that we will be able to successfully implement our business plan or successfully operate as a royalty aggregator.

We have historically been focused on discovering and developing innovative therapeutics derived from our unique platform of antibody technologies. We have now become a royalty aggregator where we focus on expanding our pipeline of fully-funded programs by out-licensing our internally developed product candidates and acquiring potential milestone and royalty revenue streams on additional product candidates. Our strategy is based on a number of factors and assumptions, some of which are not within our control, such as the actions of third parties. There can be no assurance that we will be able to successfully execute all or any elements of our strategy, or that our ability to successfully execute our strategy will be unaffected by external factors. If we are unsuccessful in acquiring potential milestone and royalty revenue streams on additional product candidates, or those acquisitions do not perform to our expectations, our financial performance and balance sheet could be adversely affected.

We may not realize the expected benefits of our cost-saving initiatives.

Reducing costs is a key element of our current business strategy. In August 2015, in connection with our efforts to lower operating expenses and preserve capital while continuing to focus on our product pipeline, we implemented a workforce reduction, which led to the termination of 52 employees during the second half of 2015. In December 2016, we restructured our business to focus our efforts on clinical development, with an initial focus on the X358 clinical program, resulting in a further reduction-in-force in which we terminated 57 employees. In early 2017, we implemented a royalty aggregator business model, which resulted in the termination of five additional employees effective June 30, 2017.

14

If we experience excessive unanticipated inefficiencies or incremental costs in connection with restructuring activities, such as unanticipated inefficiencies caused by our reduced headcount, we may be unable to meaningfully realize cost savings or capitalize on future opportunities and we may incur expenses in excess of what we anticipate. Any of these outcomes could prevent us from meeting our strategic objectives and could adversely impact our results of operations and financial condition.

Risks Related to Our Reliance on Third Parties

We rely heavily on licensee relationships, and any disputes or litigation with our partners or termination or breach of any of the related agreements could reduce the financial resources available to us, including our ability to receive milestone payments and future royalty revenues.

Our existing collaborations may not continue or be successful, and we may be unable to enter into future collaborative arrangements to develop and commercialize our unpartnered assets. Generally, our current collaborative partners also have the right to terminate their collaborations at will or under specified circumstances. If any of our collaborative partners breach or terminate their agreements with us or otherwise fail to conduct their collaborative activities successfully (for example, by not making required payments when due, or at all), our product development under these agreements will be delayed or terminated. Disputes or litigation may also arise with our collaborators (with us and/or with one or more third parties), including those over ownership rights to intellectual property, know-how or technologies developed with our collaborators.

Our licensees rely on third parties to provide services in connection with our product candidate development and manufacturing programs. The inadequate performance by or loss of any of these service providers could affect our licensees’ product candidate development.

Third parties provide services in connection with preclinical and clinical development programs, including in vitro and in vivo studies, assay and reagent development, immunohistochemistry, toxicology, pharmacokinetics, clinical trial support, manufacturing and other outsourced activities. If these service providers do not adequately perform the services for which we or our licensees have contracted, or cease to continue operations, and we are not able to find a replacement provider quickly or we lose information or items associated with our product candidates, our development programs and receipt of any potential resulting income may be delayed.

Agreements with other third parties, many of which are significant to our business, expose us to numerous risks.

Because our licensees, suppliers and contractors are independent third parties, they may be subject to different risks than we are and have significant discretion in, and different criteria for, determining the efforts and resources they will apply related to their agreements with us. If these licensees, suppliers and contractors do not successfully perform the functions for which they are responsible, we may not have the capabilities, resources or rights to do so on our own.

We do not know whether we or our licensees will successfully develop and market any of the products that are or may become the subject of any of our licensing arrangements. In addition, third-party arrangements such as ours also increase uncertainties in the related decision-making processes and resulting progress under the arrangements, as we and our licensees may reach different conclusions, or support different paths forward, based on the same information, particularly when large amounts of technical data are involved.

Under our contract with NIAID, a part of the National Institute of Health (“NIH”), we invoiced using NIH provisional rates, and these are subject to future audits at the discretion of NIAID’s contracting office. These audits can result in an adjustment to revenue previously reported, which potentially could be material.

Failure of our licensees’ product candidates to meet current Good Manufacturing Practices standards may subject us to delays in regulatory approval and penalties for noncompliance.

Our licensees may rely on third party manufacturers and such contract manufacturers are required to produce clinical product candidates under current Good Manufacturing Practices (“cGMP”) to meet acceptable standards for use in clinical trials and for commercial sale, as applicable. If such standards change, the ability of contract manufacturers to produce our and our licensees’ product candidates on the schedule required for our clinical trials or to meet commercial requirements may be affected. In addition, contract manufacturers may not perform their obligations under their agreements with our licensees or may discontinue their business before the time required by us to successfully produce clinical and commercial supplies of our licensees’ product candidates.

15

Contract manufacturers are subject to pre-approval inspections and periodic unannounced inspections by the FDA and corresponding state and foreign authorities to ensure strict compliance with cGMP and other applicable government regulations and corresponding foreign standards. We do not have control over a third-party manufacturer’s compliance with these regulations and standards. Any difficulties or delays in contractors’ manufacturing and supply of our licensees’ product candidates or any failure of our licensees’ contractors to maintain compliance with the applicable regulations and standards could increase costs, reduce revenue, make our licensees postpone or cancel clinical trials, prevent or delay regulatory approval by the FDA and corresponding state and foreign authorities, prevent the import and/or export of our licensees’ product candidates, or cause any of our licensees’ product candidates that may be approved for commercial sale to be recalled or withdrawn.

Certain of our technologies are in-licensed from third parties, so our and our licensees’ capabilities using them are restricted and subject to additional risks.

We have licensed technologies from third parties. These technologies include phage display technologies licensed to us in connection with our bacterial cell expression technology licensing program and antibody products. However, our and our licensees’ use of these technologies is limited by certain contractual provisions in the licenses relating to them, and although we have obtained numerous licenses, intellectual property rights in the area of phage display are particularly complex. If we are unable to maintain our licenses, patents or other intellectual property, we could lose important protections that are material to continuing our operations and for future prospects. Our licensors also may seek to terminate our license, which could cause us and our licensees to lose the right to use the licensed intellectual property and adversely affect our ability to commercialize our technologies, products or services.

Because many of the companies with which we do business also are in the biotechnology sector, the volatility of that sector can affect us indirectly as well as directly.

The same factors that affect us directly also can adversely affect us indirectly by affecting the ability of our partners and others with whom we do business to meet their obligations to us and reduce our ability to realize the value of the consideration provided to us by these other companies in connection with their licensing of our products.

Risks Related to an Investment in Our Common Stock

Our share price may be volatile, and there may not be an active trading market for our common stock.

There can be no assurance the market price of our common stock will not decline below its present market price or there will be an active trading market for our common stock. The market prices of biotechnology companies have been and are likely to continue to be highly volatile. Fluctuations in our operating results and general market conditions for biotechnology stocks could have a significant impact on the volatility of our common stock price. We have experienced significant volatility in the price of our common stock. From January 1, 2018, through March 4, 2019, the share price of our common stock has ranged from a high of $36.86 to a low of $11.02. Additionally, we have two significant holders of our stock that could affect the liquidity of our stock and have a significant negative impact on our stock price if one or both of the holders were to quickly sell their ownership positions.

Our results of operations and liquidity needs could be materially negatively affected by market fluctuations or an economic downturn.

Our results of operations could be materially negatively affected by economic conditions generally, both in the United States and elsewhere around the world. Concerns over inflation, energy costs, geopolitical issues, the availability and cost of credit, and the U.S. financial markets have in the past contributed to, and may continue in the future contribute to, increased volatility and diminished expectations for the economy and the markets. Domestic and international equity markets periodically experience heightened volatility and turmoil. These events may have an adverse effect on us. In the event of a market downturn, our results of operations could be adversely affected by those factors in many ways, including making it more difficult for us to raise funds if necessary, and our stock price may decline.

16

We may issue additional equity securities and thereby materially and adversely affect the price of our common stock.